Global Cryogenic Valves Market 2021-2028

November 13, 2021Global Hydrogen Gas Turbines Market 2022-2030

January 29, 2022Global Live Cell Imaging Market 2021-2028

$5195 – $7195

Growing adoption of high-content screening techniques in drug discovery and rising incidence of cancer primarily drives the market for live cell imaging. The growth in research funding and rising government funding and investment in regenerative medicine research will also support the market growth in the coming years. However, the high cost of high-content screening systems is limiting the overall adoption of these products.

| Select License Type | Single User Licence, Team Licence, Enterprise Licence |

|---|

Report Summary

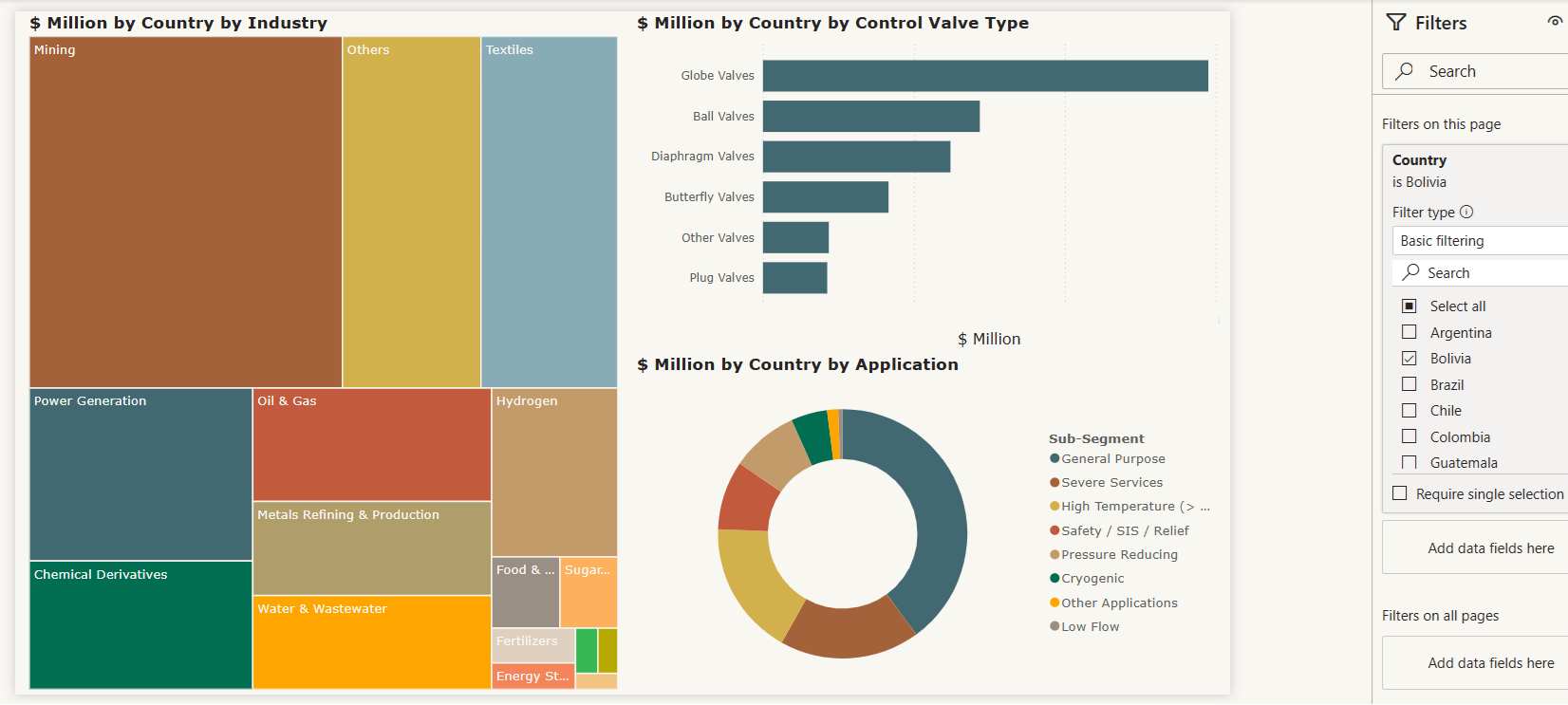

Revolutionize the way you engage with data through our cutting-edge interactive dashboard(Click to enlarge)

-

- Growing adoption of high-content screening techniques in drug discovery and rising incidence of cancer primarily drives the market for live cell imaging. The growth in research funding and rising government funding and investment in regenerative medicine research will also support the market growth in the coming years. However, the high cost of high-content screening systems is limiting the overall adoption of these products.

- Increasing funding for the development of efficient live cell imaging techniques is also anticipated to boost the market over the forecast period. Funding institutes such as Health Connexions, National Institute of Health, and W.M. Keck Foundation have granted funds to institutes such as Harvard School of Medicine, Perdue University, and Weldon School of Biomedical Engineering for the development of imaging technologies to be applied in the field of health, food, and environment.

- Shutdown measures to curb COVID-19, however, resulted in a decrease in the number of orders of biological microscopes during 2020. This has further negatively impacted the revenues of leading players operating in this market. The normalization of the global economy will slowly increase the demand for live cell imaging systems in non-COVID-related research activity labs, leading to market growth. Furthermore, players operating in the market are altering their strategies, for both long-term and short-term growth, by tapping the research market and developing innovative products to combat the pandemic. On the other hand, even though the impact of COVID-19 on the live cell imaging market is low compared to other medical device markets, timely development and implementation of contingency plans are critical for business operations and, in particular, for key imported raw materials.

Table of Content

1. Executive Summary

1.1. Market Insights

1.2. Market Outlook

1.3. Segmental Insights

2. Market Research Methodology

2.1. Research methodology and design

2.2. Sample selection

2.3. Reliability and validity

3. Market Analysis

3.1. Market size and growth rates

3.2. Market growth drivers, market dynamics and trends

3.3. Industry value chain analysis

3.4. Market scenarios and opportunity forecasts

3.5. Relevant markets

3.6. The new frontiers of growth

3.9. Emerging market needs and challenges

3.8. Industry Analysis – Porter’s

3.8.1. Threat of new entrants

3.8.2. Bargaining power of suppliers

3.8.3. Bargaining power of buyers

3.8.4. Threat of substitutes

3.8.5. Competitive rivalry

3.9. PEST Analysis

3.9.1. Political/legal landscape

3.9.2. Social landscape

3.9.3. Technological landscape

4. COVID 19 Crisis Analysis

4.1. Statistics and probable future impact

4.2. Scenarios and path forward

4.3. Sector specific impact

4.4. Industry transformation

4.5. Action plan for industry players

4.6. Supply chain: actions to consider

4.9. Initiatives prioritization

4.8. Strategic crisis-action plan

4.9. The next normal

4.9.1. Supply chain

4.9.2. Regulations

4.9.3. Organizations

5. Market Breakdown – by Component

5.1. Introduction

5.2. Instruments

5.2.1. Microscopes

5.2.2. Standalone Systems

5.2.3. Cell Analyzers

5.2.4. Accessories

5.3. Consumables

5.3.1. Reagents

5.3.2. Assay Kits

5.3.3. Media

5.3.4. Other Consumables

5.4. Software

5.5. Services

6. Market Breakdown – by Application

6.1. Introduction

6.2. Cell Biology

6.3. Developmental Biology

6.4. Stem Cell & Drug Discovery

6.5. Others

7. Market Breakdown – by Technology

7.1. Introduction

7.2. Time-lapse Microscopy

7.3. Fluorescence Resonance Energy Transfer (FRET)

7.4. Fluorescence Recovery After Photobleaching (FRAP)

7.5. High-content Screening (HCS)

7.6. Others Technologies

8. Market Breakdown – by End User

8.1. Introduction

8.2. Pharmaceutical & Biotechnology Companies

8.3. Academic & Research Institutes

8.4. Contract Research Organizations (CROs)

9.Market Breakdown by Geography

9.1. North America

9.1.1. North America Flexible Pipe Market, 2019-2028 (USD Million)

9.1.2. North America Flexible Pipe Market, by Raw Material

9.1.3. North America Flexible Pipe Market, by Application

9.1.4. North America Flexible Pipe Market, by Country

9.1.4.1. U.S.

9.1.4.2. Canada

9.1.4.3. Mexico

9.2. South America

9.2.1. South America Flexible Pipe Market, 2019-2028 (USD Million)

9.2.2. South America Flexible Pipe Market, by Raw Material

9.2.3. South America Flexible Pipe Market, by Application

9.2.4. South America Flexible Pipe Market, by Country

9.2.4.1. Brazil

9.2.4.2. Argentina

9.2.4.3. Others

9.3. Europe

9.3.1. Europe Flexible Pipe Market, 2019-2028 (USD Million)

9.3.2. Europe Flexible Pipe Market, by Raw Material

9.3.3. Europe Flexible Pipe Market, by Application

9.3.4. Europe Flexible Pipe Market, by Country

9.3.4.1. U.K.

9.3.4.2. Russia

9.3.4.3. Italy

9.3.4.4. Norway

9.3.4.5. Turkey

9.3.4.6. Denmark

9.3.4.9. Others

9.4. Asia-Pacific

9.4.1. APAC Flexible Pipe Market, 2019-2028 (USD Million)

9.4.2. APAC Flexible Pipe Market, by Raw Material

9.4.3. APAC Flexible Pipe Market, by Application

9.4.4. APAC Flexible Pipe Market, by Country

9.4.4.1. China

9.4.4.2. South Korea

9.4.4.3. India

9.4.4.4. Indonesia

9.4.4.5. Malaysia

9.4.4.6. Australia

9.4.4.9. Others

9.5. Middle East & Africa

9.5.1. MEA Flexible Pipe Market, 2019-2028 (USD Million)

9.5.2. MEA Flexible Pipe Market, by Raw Material

9.5.3. MEA Flexible Pipe Market, by Application

9.5.4. MEA Flexible Pipe Market, by Country

9.5.4.1. Saudi Arabia

9.5.4.2. UAE

9.5.4.3. Qatar

9.5.4.4. Nigeria

9.5.4.5. Angola

9.5.4.6. Tanzania

9.5.4.9. Mozambique

9.5.4.8. Others

10. Competitive Landscape

10.1. Competitive situation and trends

10.2. Company market positioning

10.3. Vendor landscape

10.4. Company geographical presence analysis

10.5. Recent market and industry developments

10.5.1. New product developments and announcements

10.5.2. Agreements, partnerships, joint ventures, and collaborations

10.5.3. Mergers and acquisitions and major PE deals

11. Company Profiles

. Company overview

. Financial performance

. Product benchmarking

. Strategic initiatives

11.1. Becton, Dickinson and Company

11.2. BioTek instruments, Inc

11.3. Bruker Corporation

11.4. Carl Zeiss

11.5. Etaluma, Inc

11.6. GE Healthcare

11.7. Leica Microsystems

11.8. Molecular Devices, LCC

11.9. NanoEntek Inc.

11.10. Nikon Corporation

11.11 Olympus Corporation

11.12. PerkinElmer, Inc.

11.13. Sigma-Aldrich Corporation

11.14. Thermo Fisher Scientific, Inc.

11.15. Others